The Australian Prudential Regulation Authority’s (APRA) recent announcement on changes to bank capital requirements could phase out bank hybrids by early 2027. Many retail investors have used bank hybrids to deliver income returns, with less risk. However with the structure potentially becoming scarce and term deposit rates declining, investors seeking steady income and franking could be forced to find alternative investment options.

To date, many self-directed and SMSF investors have seen bank hybrids as an avenue to invest into banks further ‘up the capital stack’, with the hybrid structure providing mechanisms or triggers for the banks to ‘convert’ hybrid capital to equity. Proposed changes place this at risk. Acting now by adjusting portfolios could be a wise way to help maintain similar income levels in the future.

What options may be available to investors?

In some cases, the proposed changes may see investors take additional exposure to equities, either directly through passive index tracking, or in actively managed investments. For those considering investment options that provide attractive yields and consistent fully franked income, Listed Investment Companies (LICs) offer a compelling proposition for investors.

Why LICs?

LICs have been assisting Australian investors grow wealth and earn income through for over 100 years. LICs provide easy access to professional fund managers who actively manage a range of asset classes on your behalf, with many delivering consistent income streams across a range of investment strategies, providing shareholders with access to fully franked dividends, on average higher than the franked dividend yield of the Australian equity markets.

This is achieved through the company structure of a LIC and brings many benefits to investors seeking a consistent income stream and franking credits, including:

Active choice management

The LIC manager chooses when to buy, hold or sell, and unlike index tracking investments, they have the optionality to avoid being a forced buyer in over-valued markets or a seller in falling markets. This flexibility keeps their focus on holding long-term high-quality businesses that have the ability to generate capital growth and income for shareholders.

A consistent income stream

The company structure and the historical earnings in the profits reserve enables LICs to smooth payment of dividends to shareholders and include the benefit of franking from tax paid on company profits. This avoids the ‘feast or famine’ of an open-ended trust or ETF where all income received must be paid each year and if nothing is received, nothing is paid, causing fluctuations in the income yield for investors which are generally only partially franked.

This proved to be the case during the coronavirus pandemic, where many companies reduced or did not pay dividends and most ETFs or open-ended trusts were unable to distribute income to their investors. However, many LICs were able to reward investors with stable and consistent franked dividend payments during this difficult time, with many increasing their dividend payments.

Franked income from a diverse range of asset classes

LICs can hold assets classes beyond Australian shares, including global and international equities, infrastructure, small, mid and micro-cap stocks, as well as operating strategies that specifically focus on generating income and franking.

LICs holding asset classes not usually associated with paying franked dividends can do so because they are Australian companies, making profits and paying tax in Australia. Therefore, they can attach tax paid franking credits to investor dividends like other companies, such as Commonwealth Bank of Australia (ASX: CBA), BHP (ASX: BHP) and Woolworths Group (ASX: WOW).

The time to consider LICs

LIC prices are set by individual investors. As with any other listed shares, an investor wishing to buy LICs does so on-market by bidding to match the offer of an investor wishing to sell.

Sometimes this can see LIC share prices trade ahead of more universally perceived value or fall below it. This is referred to as trading at a premium (share price above portfolio value) or a discount (share price below portfolio value).

When buying a LIC trading at a discount, investors returns are calculated on their discounted entry price. Not only could an investor be accessing a dollars-worth of underlying shares for less, their returns (including franking) would also be based on the discounted entry price.

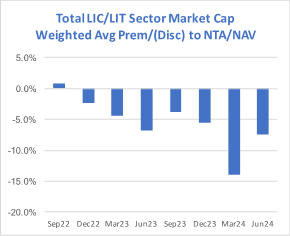

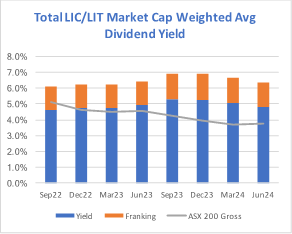

The charts below show the sector market cap weighted premium/discounts (left) and cash dividend yield (blue bars) plus franking (orange caps) on the right. Recently the sector has traded at a discount over the course of abnormally high interest rates. The ‘flip side’ is, sector cash yields plus franking are above the S&P/ASX200 index cash yield grossed up for franking (grey line), making investments in LICs an attractive proposition right now.

Conclusion

Unlike bank hybrids, the LIC structure has demonstrated enduring stability, providing consistent income streams and access to quality investment managers for over a century. The closed-end structure, with a fixed pool of capital, means portfolio managers are not forced to sell assets to meet redemptions. This allows the investment team to actively manage the portfolio and capitalise on the most compelling investment opportunities, irrespective of market conditions. With many LICs currently trading at discounts to NTA, LICs perhaps represent one of the few pockets of value left in the market.

For more information on listed investment companies, visit licat.com.au