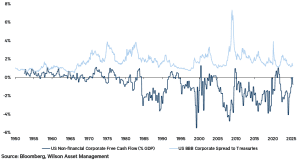

According to the Q1 U.S. Financial Accounts, corporates continue to benefit from a strong cash flow position. One preferred measure of free cash flow combines corporate internal funds with net equity issuance and subtracts capital expenditure. By design and since the 1980s, this measure is typically negative due to negative net equity issuance, or stock buy-backs. Even so, corporate free cash flow remains well above its long-term average.

This has several implications. First, despite current concerns around the U.S. labour market and capital expenditure arising from “Liberation Day” uncertainty, the starting point for corporates appears relatively strong. This financial resilience may help companies better absorb near-term turbulence. If economic activity exceeds currently subdued expectations, this could support the corporate earnings outlook. Secondly, credit spreads (the difference between corporate and government borrowing costs) typically move inversely with corporate cash flow. The current strength in cash flow aligns with the persistence of tight credit spreads from a cyclical perspective. When credit spreads are tight, it means investors are not demanding much extra return for taking on corporate credit risk.