Momentum in equity markets continued last week as stronger-than-expected earnings and evolving views on global rate cuts supported sentiment. In Australia, materials, consumer staples and healthcare outperformed during reporting season, while globally, corporate results and policy developments influenced markets. Highlights included solid results from CAR Group (ASX: CAR), Nick Scali (ASX: NCK) and RB Global (NYSE: RBA), as well as renewed strength in lithium prices following supply disruptions in China. With inflation signals still mixed, central banks balancing growth concerns, and tariff-related risks in focus, we continue to emphasise opportunities backed by structural growth, disciplined execution and exposure to long-term value creation.

Market Updates

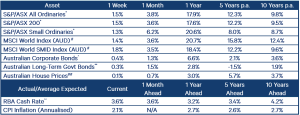

The S&P/ASX 200 Accumulation Index rose 1.5% over the week, supported by gains in materials (+3.7%), consumer staples (+2.4%) and healthcare (+2.4%). The S&P/ASX Small Ordinaries Accumulation Index also finished higher, up by 1.3%. Reporting season has so far been stronger than expected, with around one quarter of companies beating consensus earnings forecasts and 19% falling short. The RBA cut the official cash rate by 25 basis points to 3.6%, its third cut this year, while also downgrading its outlook for both growth and productivity.

In the US, the S&P 500 Index gained 1.0%, while the MSCI World Index (AUD) advanced 1.4%. Economic data was mixed: July consumer price index inflation data showed little evidence of tariff-driven inflation, raising expectations for a September rate cut, though producer price index (PPI), a separate measure of inflation that gauges price increases at the wholesale level, reaccelerated later in the week. On the policy front, President Trump signed an executive order delaying higher tariffs on Chinese imports by 90 days, pushing the deadline to 9 November.

In commodities, spodumene (lithium) prices surged another 9.9% after battery giant CATL suspended production at a major mine in China.

Key watchpoints for the week include further financial results in Australia and the US, commentary from central bankers at the Fed’s Jackson Hole Symposium, monetary policy decisions in China and New Zealand, and S&P Purchasing Managers’ Index (PMI) releases across major global economies, including Australia.

Stock Watch

CAR Group (ASX: CAR)

CAR Group, which operates online vehicle marketplaces across Australia and international markets, reported its FY2025 result last week. While the result was pre-announced, the composition of earnings and the outlook exceeded market expectations. The US macro environment for recreational vehicles has been a key concern for investors and the result confirmed there are green shoots that position FY2026 for a stronger year. Additionally, Australia’s product roadmap supports continued yield, Brazil and Korea are performing ahead of expectations and the acceleration in the US Marine market provides further upside to the US story. We are confident in the incoming CEO’s ability to continue to execute the CAR Group playbook across its geographies.

Held in: WAM Leaders (ASX: WLE), WAM Capital (ASX: WAM), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

Nick Scali (ASX: NCK)

Nick Scali, a retailer of premium furniture across Australia, New Zealand and the UK, delivered a strong FY2025 result. Performance within the Australia and New Zealand division exceeded market expectations by a wide margin, as interest rate cuts and rising consumer confidence helped buoy the local furniture market. In the UK, recently refurbished stores have shown promising early signs, supporting the potential for a broader store rollout over time. With a constructive view on the Australian and New Zealand consumer and meaningful growth opportunities in the UK, we remain positive on the company’s outlook.

Held in: WAM Capital and Wilson Asset Management Founders Fund

RB Global (NYSE: RBA)

RB Global, a leading, omnichannel marketplace for commercial assets, heavy equipment, and vehicles, delivered a strong Q2 FY2025 result, with earnings before interest, taxes, depreciation and amortisation (EBITDA) of $365 million, up 7% year-on-year. Gross Transaction Value rose 2.3%, driven by +8% growth in automotive, as IAA, RB’s recently integrated automotive salvage platform, benefited from rising total loss rates and continued market share gains. Meanwhile, activity in its commercial, construction and transportation business has remained subdued as customers adopted a wait and see approach in an uncertain macro environment. We expect this to be temporary with US interest rate cuts and clarity on tariffs likely to be positive catalysts for future growth. FY2025 EBITDA guidance was lifted to $1,340–1,370 million, with the mid-point implying 5% year-on-year growth. We increased our RB Global holding earlier in the year, taking advantage of tariff-driven market volatility.

Held in: WAM Global (ASX: WGB)

100-130 Harris Street, Pyrmont (Wentworth Capital)

In June, WAM Alternative Assets co-invested $5.0 million alongside Wentworth Capital in 100-130 Harris Street, Pyrmont, a trophy creative office asset in Sydney. The property provides a compelling rental yield, is occupied by blue-chip tenants on long-term leases and has strong environmental credentials. Wentworth Capital’s best-in-class asset management capabilities have already delivered notable improvements in upgrading the building facilities and actively managing the leasing. We are excited to gain further exposure to this high-quality real estate asset, which offers multiple value add opportunities including future rental growth, upside from the upcoming delivery of the Pyrmont metro and surrounding revitalisation, and additional development potential beyond the original investment case to increase density on part of the asset.

Held in: WAM Alternative Assets (ASX: WMA)

Platinum Capital Limited (ASX: PMC)

After the independent Platinum Capital Limited (ASX: PMC) Board had clearly articulated a path forward for the company, we were disappointed that the proposed scheme of arrangement with Platinum International Fund Complex ETF (ASX: PIXX) and then the 50% on-market buy-back were not supported by L1 Capital and its associated entities (L1 Capital). The scheme, which offered shareholders the ability to exit their investment in PMC (via PIXX) at close to net tangible asset (NTA) parity, was a culmination of almost 18 months of work by the PMC Board of Directors following a strategic review, with the primary objective of reducing the company’s share price discount to pre-tax NTA and maximising value for shareholders.

While L1 Capital supported the approval of an on-market buy-back, this support was conditional on the current Board not buying back more than 20% of the company’s shares in the period prior to the extraordinary general meeting (EGM) requisitioned by L1 Capital. In order to seek to maximise shareholder value, Wilson Asset Management has engaged the Board of PMC, submitting notices of candidature for three directors, including Geoff Wilson and proposing that Wilson Asset Management be appointed as investment manager. Under the terms of the Wilson Asset Management proposal, we would look to fully utilise the 50% on-market buy-back, in line with the current Board’s original proposal, as well as honouring the current fee arrangement, including the recoupment of the aggregated underperformance of PMC with respect to the performance fee calculation.

We look forward to working proactively with the current Board and shareholders as they consider Wilson Asset Management’s proposal, which we believe is on more favourable terms compared to L1 Capital’s proposal.

Held in: WAM Strategic Value (ASX: WAR)

Be mindful of accelerating US goods inflation

The US consumer price index (CPI) report for July revealed an acceleration in “super-core” services inflation but relatively benign goods inflation. Investors do not appear particularly anxious about inflation, with pressure building on the Fed to cut rates. While services remain the main driver of inflation given their weight in the economy, tariffs have shifted attention to goods where no significant spike has yet emerged, even now, several months after “Liberation Day”.

However, the PPI points to material goods inflation that is yet to flow through to the official CPI numbers, running 17% ahead the goods CPI and widening in recent months, consistent with growing pipeline inflation pressure. Since the PPI excludes the direct effects of tariffs as they are not retained by producers as revenue, it likely understates underlying pressure.

Historically, US companies have offset higher goods prices by restraining labour costs relative to productivity, but may become more challenging amid tight labour markets and slowing labour supply growth from migration. The risk is that goods inflation reaccelerates over the next year, complicating the case for aggressive rate cuts which are generally supportive for equities.

Index returns performance table

To stay informed with our regular updates and market insights from the team follow our LinkedIn, X and Facebook accounts.

You can also follow Wilson Asset Management Founder and Chairman Geoff Wilson AO on X and LinkedIn.

If you have any feedback you would like to share or wish to speak to a member of the Wilson Asset Management team, please respond to this email or call Christopher Ball on 02 9247 6755. You can also email us at info@wilsonassetmanagement.com.au.

Join our community of more than 90,000 weekly readers and subscribe to our regular investment insights and market updates: https://wilsonassetmanagement.com.au/subscribe/