Equity markets were driven last week by discussion of potential US rate cuts, tariff developments and a continuation of reporting season. In Australia, the ASX 200 was supported by strength in consumer discretionary, financials and communication services stocks. Globally, US Federal Reserve (Fed) Chair Jerome Powell’s comments at Jackson Hole fuelled optimism for September easing, while European and US trade talks brought progress on tariffs. With inflation still mixed and the possibility of liquidity challenges ahead, we continue to emphasise structural growth, disciplined execution and companies positioned for long-term value creation.

Market Updates

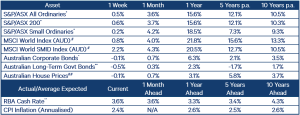

The S&P/ASX 200 Accumulation Index rose 0.6% over the week, supported by gains in consumer discretionary (+3.8%), financials (+3.5%) and communication services (+3.4%). The S&P/ASX Small Ordinaries Accumulation Index also finished higher, rising 0.2%.

On Thursday, the ASX 200 surpassed 9,000 points for the first time, driven by a strong reporting season, interest rate cuts and easing global trade concerns. Earlier in the week, the Albanese government hosted a three-day summit in Canberra with business, unions and policymakers to address Australia’s productivity. Meanwhile, consumer confidence hit a three-and-a-half-year high, ending what Westpac called a “long period of pessimism.”

In the US, the S&P 500 ended the week up 0.3%, rebounding on Friday’s rally after four consecutive days of losses. The S&P Small Cap 600 climbed 3.5%, while the MSCI World Index (AUD) gained 0.8%.

Fed Chair Powell signalled the central bank could begin cutting rates as soon as September (explored further below). The US extended steel and aluminium tariffs to 407 additional product categories, with a 50% duty now covering about US$325 billion in imports (up from US$191 billion previously). S&P Global reaffirmed the US credit rating at AA+, one notch below AAA, supported by US$21 billion in July tariff revenue. The rating helps keep borrowing costs lower and underpins confidence in US debt. S&P expects the fiscal deficit to narrow to about 6% of GDP this year, down from 7.5% in 2024.

In the UK the annual inflation rate climbed to 3.8% in July, an 18-month high and the highest in the G7, driven by rising transport, energy and accommodation costs alongside a tight labour market.

In commodities, spodumene (lithium) prices surged another 20.2%, up 47.6% over the past month, with some traders taking profits following warnings that China will unwind supply cuts in the coming months, leaving the physical market stuck in a surplus.

Key watchpoints this week include Chinese PMI readings which provide a measure of the health of the manufacturing and services sectors, and Nvidia’s (NASDAQ: NVDA) result in the US on Thursday. Domestically, we will be reviewing the RBA’s policy meeting minutes, with expectations building for a rate cut next month.

Stock Watch

Seek (ASX: SEK)

Seek, operator of Australia’s leading online employment marketplace, reported its FY2025 result last week. We increased our position ahead of the result, on the belief that the Australian job market was stabilising and showing early signs of improvement, while the share price had yet to reflect this. The May investor day marked an inflection point: the end of a downgrade cycle and a return to growth, with guidance upgraded to the top end of the range. Last week’s result continued this momentum. With supportive macro conditions, strong fundamentals and a clear valuation gap relative to online classifieds peers, we believe Seek is well positioned for share price growth.

Held in: WAM Leaders (ASX: WLE), WAM Income Maximiser (ASX: WMX) and Wilson Asset Management Leaders Fund

SRG Global (ASX: SRG)

SRG Global, an Australian diversified infrastructure services company spanning maintenance, industrial services, engineering and construction, reported a strong FY2025 result with underlying earnings per share up 34% year on year. In late June, SRG secured $850 million in contract awards and extensions across 15 projects, all with blue-chip, repeat clients across a wide range of sectors. Looking ahead, the company has guided to FY2026 EBITDA growth of around 10% which could be conservative given its 80% earnings visibility, strong track record, and recent contract wins. We continue to see upside from earnings growth and potential mergers and acquisitions opportunities.

Held in: WAM Capital (ASX: WAM) and WAM Active (ASX: WAA)

Edwards Life Sciences (NYSE: EW)

Edwards Lifesciences, a global leader in medical innovations for heart disease, last week announced an accelerated US$500 million share buyback, bringing total buybacks in 2025 to more than US$800 million. The programme is being funded from existing cash and signals to the market that management believes the stock is undervalued. We expect the company to continue its strong 1H outperformance while proactively managing costs and discretionary spending. We continue to hold Edwards given the multiple catalysts over the coming years that support its growth targets, including indication expansion (securing approval to use the same product in additional areas), greater market penetration, and new product launches.

Held in: WAM Global (ASX: WGB)

Healthcare Australia (Crescent Capital Partners)

Healthcare Australia (HCA) is Australia’s leading provider of recruitment, NDIS and care services and training. HCA, owned by our investment partner Crescent Capital Partners (Crescent), connects healthcare professionals, organisations and people to provide end-to-end healthcare solutions. Guided by the expertise of the team at Crescent, HCA has increased market share and generated strong revenues, underpinned by long-term contracts with government departments and healthcare organisations. In July 2025, WMA benefitted from an upwards revaluation of HCA driven by recent earnings growth and a continued positive outlook.

Held in: WAM Alternative Assets (ASX: WMA)

Powell says rate cuts may be appropriate

At the Jackson Hole Symposium, Fed Chair Powell has said that rate cuts may be appropriate given fragility in labour markets, and the prospect of tariffs gradually passing through to consumers such that inflation pressures remain muted. Regarding the labour market, Powell has suggested that the US has entered an unusual phase where both labour demand and supply have softened at the same time. While this leaves the unemployment rate low, he noted that such a phase indicates a more fragile labour market with downside risks to job creation. Further, without a sufficiently tight labour market, Powell expressed scepticism that tariffs and inflation expectations would feed into higher future inflation via the wage bargaining process. In response, bond yields fell and equities rallied strongly. Doves interpreted Powell as endorsing a September rate cut, while hawks argued that he merely paved the way for more active debate.

WAM Alternative Assets (ASX: WMA) Meet The Manager

We invite you to meet with Portfolio Manager Nick Kelly, Investment Analyst Jacob Grover and Investment Specialist Martyn McCathie for an exclusive in-person presentation on the WAM Alternative Assets investment portfolio, followed by a complimentary morning tea.

Register using the following links:

Brisbane | Wednesday, 3 September 2025

Adelaide | Wednesday, 10 September 2025

Melbourne | Wednesday, 17 September 2025

October Shareholder Presentations

The Wilson Asset Management and Future Generation teams look forward to meeting with shareholders at our upcoming Shareholder Presentations in October. Meet the Wilson Asset Management investment team to hear their market outlook, high-conviction stock picks and discuss some of the key themes influencing the investment portfolios. Learn more about the Future Generation companies and how they invest for impact, delivering both investment and social returns for shareholders.

Register using the following links:

Newcastle | Thursday, 16 October 2025

Gold Coast | Tuesday, 21 October 2025

Toowoomba | Wednesday, 22 October 2025

Noosa | Thursday, 23 October 2025

Index returns performance table

To stay informed with our regular updates and market insights from the team follow our LinkedIn, X and Facebook accounts.

You can also follow Wilson Asset Management Founder and Chairman Geoff Wilson AO on X and LinkedIn.

If you have any feedback you would like to share or wish to speak to a member of the Wilson Asset Management team, please respond to this email or call Christopher Ball on 02 9247 6755. You can also email us at info@wilsonassetmanagement.com.au.

Join our community of more than 90,000 weekly readers and subscribe to our regular investment insights and market updates: https://wilsonassetmanagement.com.au/subscribe/