Last week’s surprise decision by the Reserve Bank of Australia (RBA) to keep rates on hold had clear impacts on the Australian equity market, and New Zealand’s Reserve Bank followed suit. Portfolio Strategist Damien Boey wrote a piece for Livewire Markets off the back of the decision, which you can read here.

June 2025 Investment Update

Today we announced our June 2025 investment update for all of our listed investment companies.

- WAM Capital (ASX: WAM)

- WAM Leaders (ASX: WLE)

- WAM Global (ASX: WGB)

- WAM Microcap (ASX: WMI)

- WAM Alternative Assets (ASX: WMA)

- WAM Strategic Value (ASX: WAR)

- WAM Research (ASX: WAX)

- WAM Active (ASX: WAA)

- WAM Income Maximiser (ASX: WMX)

Market Updates

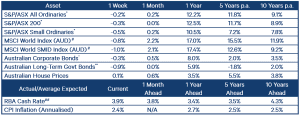

The S&P/ASX 200 Accumulation Index fell 0.3% over the week, driven by softness in real estate (-3.2%), information technology (-2.0%) and consumer staples (-1.9%), and partly offset by strong gains in utilities (+3.4%). The S&P/ASX Small Ordinaries Accumulation Index also finished 0.5% lower.

On Tuesday, the Reserve Bank of Australia surprised markets by leaving the cash rate unchanged at 3.85%, a decision widely viewed as a prelude to an August cut pending the outcome of second quarter consumer price index (CPI) to be released on 30 July. The Reserve Bank of New Zealand also held its cash rate steady on Wednesday.

Major U.S. benchmarks finished modestly lower, with the price change for the S&P 500 (large caps) and the S&P Small Cap 600 (small caps) declining 0.3% and 0.2% respectively. Despite gains in Europe, the MSCI World Index (AUD) declined 0.8%. While markets focused on tariff news, the reaction was muted compared with previous tariff announcements on the view that Trump would seek a negotiated outcome. Specifically, 30% tariffs on the European Union and Mexico, 25% on major trading partners South Korea and Japan, as well as tariffs at varying levels on other countries, including Canada, South Africa, Thailand, and Malaysia were announced. All are scheduled to take effect on 1 August unless a trade deal is reached before then.

Most commodities strengthened, with U.S. copper prices jumping over 10% after U.S. President Donald Trump threatened a 50% tariff on the metal, matching his existing tariffs on steel and aluminium imposed earlier this year. The U.S. also flagged 200% tariffs on pharmaceutical imports within 18 months, which the Australian government estimates could affect up to $2 billion worth of pharmaceutical exports.

Key watchpoints for the week ahead include Chinese economic data today and Tuesday, and U.S. inflation prints on Tuesday.

Stock Watch

Real Estate Investment Trusts (REITs)

The real estate investment trusts (REITs) sector traded softly last week after the Reserve Bank of Australia’s surprise decision to leave the cash rate unchanged. This pushed the Australian Government bond yield curve (the line plotting yields across maturities) upwards, putting pressure on rate-sensitive sectors such as property. The pull-back presented an opportunity to increase our positioning in selected names that we believe are well placed to deliver value for shareholders. Our preferred exposure includes Goodman Group (ASX: GMG), Charter Hall Group (ASX: CHC) and GPT Group (ASX: GPT).

Held in: WAM Leaders, WAM Income Maximiser and Wilson Asset Management Leaders Fund

Summerset Group Holdings

Summerset, a developer and operator of integrated retirement villages and aged-care facilities across New Zealand, delivered a strong Q2 2025 trading update last week that revealed green shoots after a softer Q1 2025. New sales were the standout, rising 42% year on year and coming in 16% ahead of consensus expectations. We added to our position ahead of the update and were encouraged by the company’s strong execution.

Held in: WAM Capital, WAM Research and WAM Active

Lottomatica (BIT: LTMC)

Lottomatica, operator of Italy’s largest integrated gaming platform, traded strongly last week after repurchasing €11.6 million of stock (0.20% of shares on issue), demonstrating execution of its previously announced €500 million share buy-back. This followed an announcement in early July that private equity firm Apollo had successfully exited its holding in the company, removing the overhang from a sell-down and broadening the share register. We believe Lottomatica has a robust medium-term opportunity, supporting revenue growth and operating efficiency.

Held in: WAM Global

Australian water entitlements (Argyle Group)

WAM Alternative Assets invests in a portfolio of high-security Australian water entitlements through our investment partner Argyle Group. Water entitlements are permanent legal rights to access a share of water from specific rivers or aquifers, which underpin the long-term productivity of land, support regional economic resilience and offer investors access to a stable, real asset with strong long-term fundamentals. With the water year resetting in July, entitlement holders received new allocations of water, which can be leased and sold forward to generate income for investors. We expect to see long-term capital growth from water entitlements as structural changes to supply increase scarcity.

Held in: WAM Alternative Assets

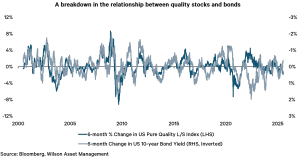

A breakdown in the relationship between quality stocks and bonds

High quality companies in the equity market are those that justify having a high price-to-book multiple. By definition, they offer superior profitability, payout, safety and growth. Historically, investors have tended to favour quality companies when bond yields fall, because lower yields are typically a sign of slowing economic growth, consistent with investors looking for more defensiveness in their portfolios. However, it is interesting to note that over the past few quarters, bond yields have fallen – but high-quality stocks have underperformed low-quality stocks. This is a very unusual relationship breakdown. What it implies is that at present, investors see bonds as a source of risk, rather than a safehaven against it.

In the absence of an imminent, recessionary shock, we think that there are limits to how far bond yields can fall, because lower yields are easing financial conditions and supporting the cycle. Further, if bond yields rise a little, they may still be at levels supporting economic growth, and equity valuations. The major concern would be if bond yields rise a lot, undermining the valuations of expensive stocks. A sharp rise in bond yields could occur if we see significant de-leveraging in the hedge fund and primary dealer space. Fortunately, for equity and bond investors, this is not the evidence being presented just yet, with central bankers also keen to avoid this outcome.

Index returns performance table

To stay informed with our regular updates and market insights from the team follow our LinkedIn, X and Facebook accounts.

You can also follow Wilson Asset Management Founder and Chairman Geoff Wilson AO on X and LinkedIn.

If you have any feedback you would like to share or wish to speak to a member of the Wilson Asset Management team, please respond to this email or call Christopher Ball on 02 9247 6755. You can also email us at info@wilsonassetmanagement.com.au.

Join our community of more than 90,000 weekly readers and subscribe to our regular investment insights and market updates: https://wilsonassetmanagement.com.au/subscribe/