By Joyce Moullakis and Joanne Tran

Investment bankers are optimistic they can fire up a sluggish market for initial public offerings in 2026, despite fund managers questioning whether the prospect of interest rate rises and unrealistic price expectations will keep a lid on activity.

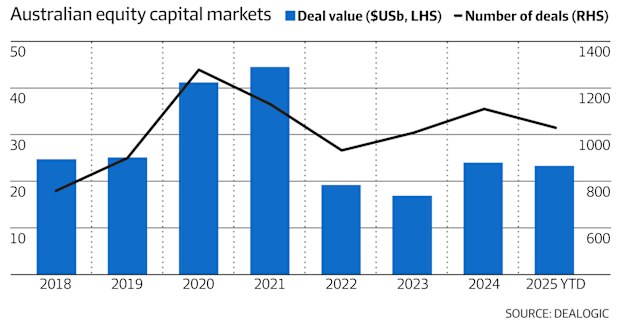

The volume of initial public offerings dipped to $US2.42 billion ($3.6 billion) in 2025, according to Dealogic data as at December 24. That tally compared to $US2.48 billion in the prior year, and remained markedly below the annual average over the last decade of $US3.15 billion.

The largest ASX listings in 2025 were those of over-50s resort living provider GemLife, airline Virgin Australia and gold producer Greatland Resources respectively.

While those stocks are still trading above their offer prices, the underwhelming performance of new listings in the latter weeks and months of 2025 has dented investor sentiment, and cast a pall over the bulging 2026 IPO pipeline.

The crop of 2025 floats that are still trading well below their respective offer price include medical device company Saluda Medical, Cochlear-backed Epiminder and used car retailer Carma.

WAM Capital portfolio manager Oscar Oberg questions whether the macroeconomic environment will be conducive to a bumper 2026 for ASX listings.

“The pipeline has been large for some time, but uncertainty around interest rates at present will likely delay some of these intended IPOs,” he said.

TenCap portfolio manager Jun Bei Liu agreed that the changing rate environment was likely to hinder IPO activity.

“Valuations are the biggest challenge for IPOs [in 2026],” she said. “There’s a wide gap between what issuers want and what investors are prepared to pay in a potentially higher rates environment.

“Over the past three months, sentiment has taken a hit as the recent IPOs have performed poorly. It inevitably makes investors more cautious.”

Still, investment bankers, who are typically upbeat on the outlook for transactions, are confident 2026 will see an upswing in equity capital markets deal flow and ASX listings.

The runway for sharemarket listings has been looking more crowded, helping to underpin some of that optimism. It includes artificial intelligence infrastructure company Firmus Technologies, Home Furniture Group, which houses Amart and Freedom, radiology business I-MED, and pets-and-vets business Greencross.

“IPO momentum is building particularly in technology and AI,” said Justin Grimmond, JPMorgan’s head of equity capital markets.

“More broadly across deal flow we expect the technology, digital infrastructure and natural resources sectors to continue to be very active.”

Local investors are also closely watching to see whether e-commerce software firm Rokt and design giant Canva pursue Nasdaq listings in 2026. Float deliberations at Rokt have included assessing plans to simultaneously list on the Nasdaq and the ASX and, given a hollowing out of the latter, it would be welcomed.

“The volume of private capital will continue to impact [the] ASX through reduced IPO activity and ongoing take-private activity,” said Charlie Daish, UBS’s head of ECM origination, noting a healthy 2026 IPO pipeline.

Australia’s still-soft market for floats has contrasted with a hive of IPO activity in the United States. Medical supply behemoth Medline listed on the Nasdaq in December after raising $US6.26 billion, and bumper 2025 US activity also included the floats of design software firm Figma and artificial intelligence infrastructure group CoreWeave.

In 2025, Australia’s corporate regulator tried to address the dwindling number of new ASX-listings relative to companies pursuing trade sales or private capital for growth. It released a sweeping report on public and private markets and a host of measures and potential reforms in an attempt to jumpstart the market for floats.

Measures included trialling a fast-track route for IPOs, making dual listings for foreign companies easier, cutting the amount of documentation needed and providing more flexibility around financial forecasts.

John McLean, Citi’s head of asset managers and ECM, said while the firm was seeing a noticeable increase in proposals from companies seeking to list in 2026, positive share price performance from IPOs was key to boosting confidence in the market.

“Successful post-listing performance will be the most potent catalyst for restoring confidence in IPO markets,” he added.

McLean also noted the potential inclusion of an IPO candidate in a sharemarket index was dominating float-related questions and preparations.

”The introduction of mandated annual performance testing of super funds under the ‘Your Super, Your Future’ legislation is changing the Australian investor landscape,” he said. “Super funds are particularly sensitive to achieving benchmarked returns, which has acted as a deterrent to participating in IPOs where the risk is higher.“

Morgan Stanley’s head of ECM Luke Boeg said including a listing candidate in an index meant broader fund manager ownership, as passive funds accounted for about 15 per cent of an ASX company’s shareholder register.

“As a constituent of the key indices, a company can benefit from these fund flows and become more relevant to a significantly wider set of investors,” he added.

In the ECM league tables for Australia, JPMorgan topped the 2025 rankings, followed by Canaccord Genuity and Barrenjoey/Barclays. That includes IPOs and follow-on raisings for growth capital and mergers and acquisitions.

Total ECM activity in Australia amounted to $US23.3 billion in 2025, down from $US24 billion the prior year.

Boeg said he was “increasingly constructive” on the outlook for mergers and acquisitions and growth-related funding.

“Merger and acquisition activity was benign in 2025, but this is turning, and with it we should see a pick-up in issuance to support this,” he added.

Licensed by Copyright Agency. You must not copy this work without permission.